3 Minute Read

For income investors, nothing is more deflating than the tax bite. A well-planned income strategy may look good on paper, but loses some of its luster once that income is taxed.

The after-tax frustration is why many income investors pursue municipal bonds, which are exempt from federal taxes, as part of their income strategy. But investors should also consider real estate for income needs, as the asset class has more levers to pull when it comes to reducing the tax bite.

This blog is the second in a series looking at the tax advantages of real estate investing. (Our first blog, on 1031 exchanges, can be found here.) In this post, we look at cost segregation, an accounting treatment that allows investors to realize a greater portion of tax deductions through realizing accelerated depreciation of real estate in the early years of ownership. In many cases, this can increase the investment’s cash flow by thousands of dollars up front.

As we explain in this blog, recent adjustments to the tax code have made cost segregation a more valuable tool for increasing after-tax income.

What is Cost Segregation?

Cost segregation is easy to conceptualize. When an investor makes an investment in real estate, they can depreciate the asset over time. The annual amount of depreciation can be used to offset the taxable income paid on the investment. As a simple example, if a property yields $15,000 in income, but the property is depreciated by $5,000 that year, the investor only pays taxes on $10,000 of the annual income.

So how does cost segregation help? It allows the investor to accelerate depreciation of many assets associated with the investment, realizing tax benefits sooner. Traditionally, non-residential commercial real estate is depreciated over the course of 39 years, while a residential rental property depreciates over 27.5 years. That’s a long period to slowly realize tax savings from depreciation – most real estate investors are unlikely to hold the property that long.

Cost segregation allows the investor to group assets associated with the property into different buckets that have different depreciation schedules. These different buckets can have a five-, seven-, 15- or 39-year depreciation schedule. By breaking down the investment property into components with shorter tax lives, the investor dramatically increases the tax deductions taken in the early years of the investment.

How Much Can Cost Segregation Help?

The benefit from cost segregation will vary for every single property, based on the amount of assets that are assigned to different depreciation schedules. But at Forum, we’ve seen that the cost segregation process has allowed us to increase depreciation expense by at least 20% annually over the first 10 years.

A simple, back-of-the-envelope example, courtesy of the CCIM institute, shows how substantial the savings can be. The example looks at the early, added depreciation expenses an investor adds when using a cost segregation study for a $1.3 million property.

If no cost-segregation study is performed, the taxpayer enters the cost into the fixed-asset system as 39-year property. After the first five years, the taxpayer has accumulated $154,622 in depreciation expenses. However, consider the same property using cost segregation. After thorough engineering analysis combined with an understanding of what qualifies as short-life property as defined by Internal Revenue Code Section 1245, the (property) is reclassified into five-year ($260,524), 15-year ($348,590), and 39-year ($718,457) property. After the first five years, the taxpayer has a total of $460,545 in accumulated depreciation expense.

The obvious difference is that the taxpayer has increased the accumulated depreciation expense by $305,000. With a cost-segregation study, the taxpayer has taken the majority of his depreciation up front and realizes that a dollar saved in the first five years is worth more than the same dollar in 16 years. As a result, the taxpayer has a net present value savings of almost $100,000.

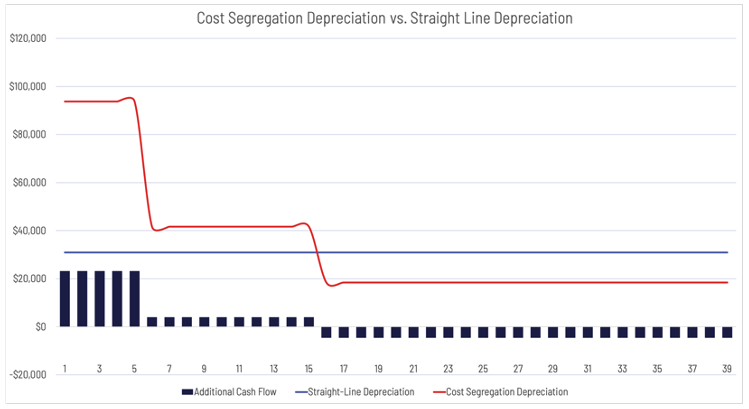

The graph below puts the example from the CCIM Institute into perspective. The orange line shows the depreciation amount each year after the property has been reclassified. The green bars show the additional cash flow this method provides the investor in the early years as he or she increases depreciation to minimize the amount of income from the property that is taxed.

“The obvious difference is that the taxpayer has increased the accumulated depreciation expense by $305,000. With a cost-segregation study, the taxpayer has taken the majority of his depreciation up front and realizes that a dollar saved in the first five years is worth more than the same dollar in 16 years. As a result, the taxpayer has a net present value savings of almost $100,000.”

Recent Tax Code Changes Make Cost Segregation a More Valuable Tool

Recent tax law changes under the Tax Cuts and Jobs Act of 2017 (“TCJA”) have given a boost to cost segregation. Previously, tax law allowed property owners to take a “bonus depreciation” of 50% in the investment’s first year. In simple terms, this meant certain assets could forego their regular depreciation schedule, and instead, investors could recognize 50% of the asset’s total depreciation in the first year. New tax law has increased the bonus depreciation to 100% for qualifying .

The 100% deduction only lasts until 2022, and will be phased out by 2027.

What to Know Before Starting

While the early year tax savings from cost segregation are significant, the analysis requires professional help. Property owners typically utilize a CPA and engineer to produce a cost segregation study. Here are a few things to consider so that you are prepared to take advantage of the cost segregation method:

1. Conduct the analysis soon after purchase. A cost segregation analysis must be conducted in the first year of purchase to receive maximum benefit.

2. Don’t wait until the end of tax season. Due to the complexity of cost segregation analysis, this is not something an accountant can tackle in the final weeks of tax season.

3. Use a reputable expert. Rely on an expert firm that has done plenty of cost segregation studies. By using a reputable firm with prior experience, investors have someone to fall back on if the IRS questions how assets were grouped.

4. Ask for a cashflow analysis. You deserve to see how the cost segregation treatment is improving cashflow from the property in the early years.

5. Ask your advisor and accountant about tax changes. Changes in bonus depreciation levels from the TCJA have meant considerable savings for property investors.

Real Estate Offers Income Investors Ample Room to Reduce the Tax Bite

The tax advantages from cost segregation highlight one of the ways property investors can reduce the tax burden of their income, but cost segregation is only a piece of the puzzle. Utilizing a 1031 exchange can also increase the after-tax income associated with a property.

A combination of these tools makes real estate one of the most advantageous income investments from a tax perspective, and is why we believe it has a rightful place in the portfolios of most income-seeking investors.

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Forum Investment Group is a private real estate investment firm with expertise and emphasis on generating current income and long-term value creation by accessing unique real estate acquisition, development and debt investment opportunities across the capital stack and real estate cycles. Since 2007 we’ve invested more than $2 billion in real estate and built a successful track record of high-performance investments, earning the trust of our investors and partners.

Need help taking advantage of cost segregation? Forum takes care of many of the steps for you.

![]()

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

John Kolstoe – Managing Director – Finance

jkolstoe@forumre.com

DISCLOSURE:

The materials to which this disclosure is attached as well as any electronic or verbal communication related to the subject matter of these materials are intended for informational purposes only, are subject to change, and do not constitute investment advice or a recommendation to you. Such an offer to sell or solicitation to buy an interest in the Fund may be made only by the delivery of the Fund’s Confidential Private Placement Memorandum (the “Memorandum”) specifically addressed to the recipient thereof. In the event that these materials and the Memorandum are conflicting, the Memorandum’s terms shall control. Please review the Memorandum fully and consult with your legal and tax counsel, as appropriate. All documents should be reviewed carefully by you and your financial, legal, and tax advisors. Any product or service referred to herein may not be suitable for all persons. This information is intended solely for institutional investors/consultants, foundations and endowments as well as for “accredited investors” (as defined by the Securities and Exchange Commission (“SEC”) under the U.S. Securities Act of 1933, as amended). Any reproduction of these materials, in whole or in part, or the divulgence of any of the contents, is strictly prohibited (excepting that the tax treatment and tax structure of any Fund may be disclosed as necessary), except to the extent necessary to comply with any applicable federal or state securities laws. These materials are intended for the exclusive use of the designated recipients and may not be reproduced or redistributed in any form or used to conduct any general solicitation or advertising with respect to any Fund or investment discussed in the information provided. The Fund has not been registered or qualified with, nor approved or disapproved by, the SEC or any other regulatory agency nor has any regulatory authority passed upon the accuracy or adequacy of any information that has been or will be provided. In addition to restrictions on the transference of an investor’s interest in the Fund, there is no secondary market for the Fund, and none is expected to develop. Fees and expenses may offset the Fund’s portfolio’s trading profits. Although the Fund or investment professionals managing it may have a significant track record, this type of investment should be considered speculative and involves a high degree of risk. All materials are meant to be reviewed in their entirety, including footnotes, legal disclaimers, and any restrictions or disclosures. Past performance is no guarantee of future returns. The Fund’s performance may be volatile, and the investment may involve a high degree of risk. The Fund is intended only for sophisticated investors who meet the investor suitability requirements described in the relevant Memorandum and who can bear the risk of investment losses, including the potential loss of their entire investment.

Leave Comment